Collateralized Loan Obligation Risks and Ratings Explained

BY NICK J. EVANS

CM Wealth ASSOCIATE DIRECTOR OF INVESTMENTSDisciplined, research-led allocation: CM Wealth conducts deep due diligence and selectively partners with specialized managers to identify strategies that align with client-specific risk and return goals.

Tactical positioning driven by market dislocations: CM Wealth actively monitors markets to opportunistically deploy capital when relative value improves.

Purpose-built portfolio integration: CLOs are incorporated only when they serve a defined role, whether as a cash-plus solution, equity alternative, or yield enhancer—all tailored to each client’s broader allocation strategy.

Over the past decade, the collateralized loan obligation (CLO) market has experienced substantial growth, enhancing liquidity and attracting a diverse investor base. These financial instruments pool large portfolios of corporate loans, aiming to offer investors a range of risk and return options.

CLOs do not move in lockstep with the broader stock or bond markets. They also pay floating interest rates. As interest rates increase, the coupon paid by the CLO rises, seeking to maintain its market value and providing a natural hedge against inflation. CLOs have near-zero duration, meaning their prices are relatively insensitive to interest rate changes. This combination adds diversification and may enhance wealth preservation.

CM Wealth’s approach to CLOs broadly reflects our investment philosophy. We perform thorough due diligence, evaluate specialized managers, and tactically allocate to attractive strategies based on our perceived risk-reward tradeoff compared to other asset classes. When appropriate, we incorporate this asset class into client portfolios in a targeted manner.

What are CLOs, and How Are They Structured?

Think of a CLO as a company created solely to hold loans and pay investors. A CLO entity raises capital by selling tranches of securities to investors—from the most senior, highest-rated debt (typically AAA rated) down to an unrated equity tranche. It uses this money to purchase a diverse portfolio of loans (often 100–300 different loans) made to businesses across various industries. These loans are generally first-lien senior secured loans, meaning they are backed by borrower collateral and have the first claim on assets if a borrower defaults. The loans pay interest to the CLO, which in turn is used to pay investors in the CLO’s tranches.

Tranches and Cash Flow Waterfall

Each tranche has a different priority in receiving interest and principal from the underlying loans:

Senior tranches (AAA, AA, A): Receive payments first, carry lower risk, and pay lower yields. No AAA tranche has ever lost principal.

Mezzanine or junior debt tranches (BBB, BB, B): Paid after seniors, moderate risk, higher interest rates.

Equity tranche (unrated): Last in priority, highest potential return, highest risk. Equity investors get whatever cash remains after all the debt tranches are paid.

If some loans in the pool default or underperform, losses hit the lowest tranche (equity) first and move upward only if lower tranches are completely wiped out. For example, if 5% of loans default and cannot be recovered, the equity investors bear that loss; senior debt holders remain unaffected.

CLOs also have built-in interest coverage and overcollateralization tests. If these tests fall below required levels (say, due to loan defaults), then cash that would normally go to equity is redirected to repay senior debt and shore up the structure. These mechanisms help protect investors in higher tranches.

From Cash Complement to Equity ‘Alternative’

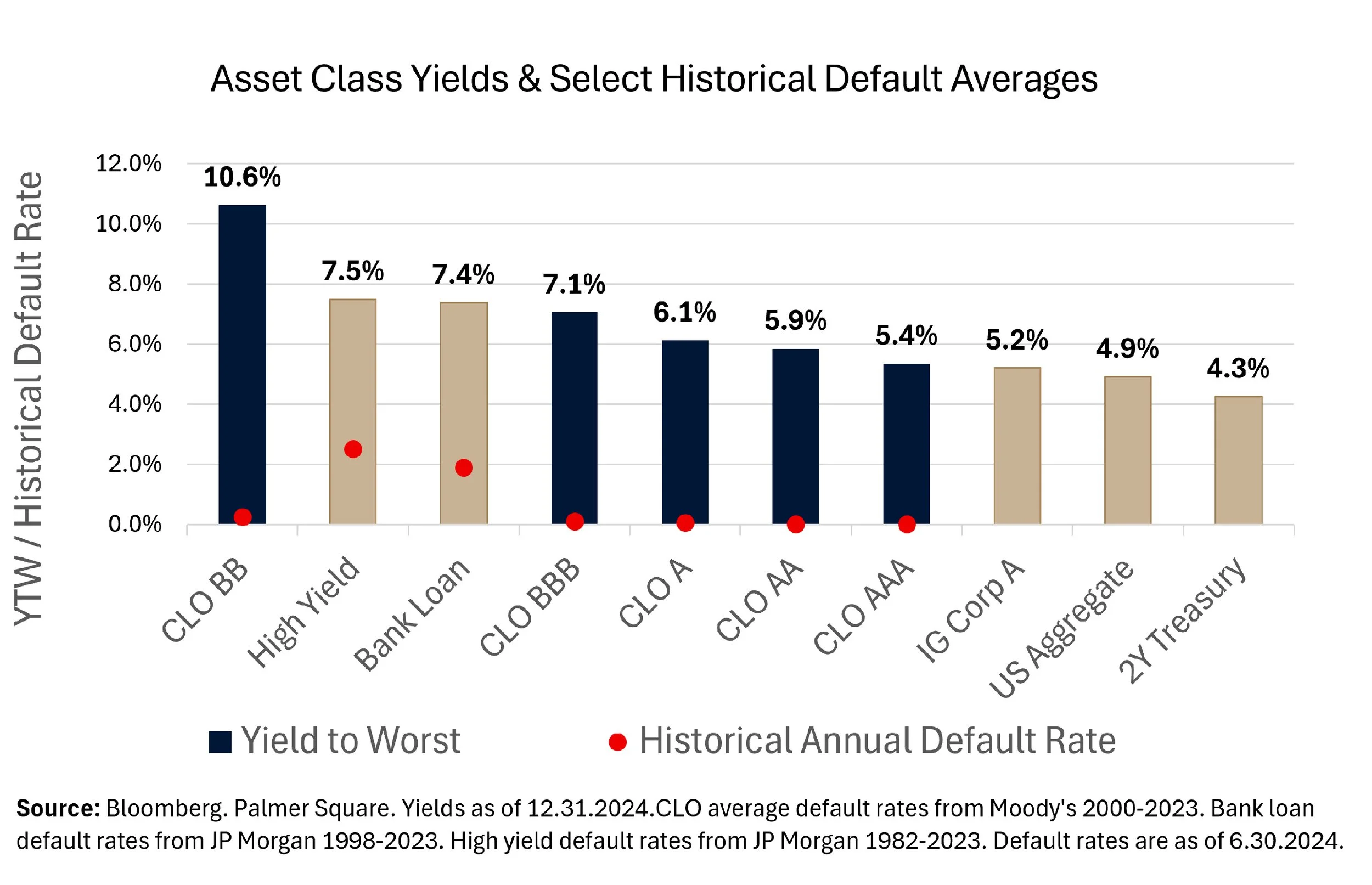

CLOs offer attractive returns, often paying higher yields than comparable bonds, with low default rates on rated tranches. For investors who seek steady income (to fund lifestyles, trusts, or philanthropic activities), this extra yield can be meaningful.

Over the past 3-5 years, publicly traded CLO funds (ETFs and interval funds) have become popular. We have strategically utilized these liquid funds, focusing on top-rated tranches, as a cash-plus complement. The highest-rated tranches are the most liquid; no AAA tranche has ever been impaired, and today, top-rated CLO ETFs yield ~5.5% (versus the 3-month U.S. treasury rate of ~4.3%).

CLO equity tranches can potentially deliver even higher returns (mid to upper teens in favorable scenarios), making them akin to an “alternative” investment with equity-like upside and more volatility. We recently added a diversified CLO fund within our Defensive Strategies Partnership to improve an existing position and complement the existing strategies. Managed by a knowledgeable and experienced team, it can opportunistically allocate across CLO tranches, from AAA to equity. This flexible credit strategy offers equity-like returns and diversification, downside protection, low-interest rate duration, relatively high yield, and low correlation to broad equity and fixed income indices. This strategy’s current yield is north of 12%, as of June 2025.

Tactical Implementation in CM Wealth Portfolios

We constantly evaluate the risk-reward tradeoff of these strategies and how they complement existing allocations. For instance, when credit spreads widened (approximately two years ago), we added a CLO mezzanine debt (BBB-B) focused strategy where appropriate. In our view, adding CLO debt to a balanced portfolio enhanced the overall yield without a proportionate increase in portfolio risk.

Base interest rates had risen, mezzanine CLO debt spreads widened, and these tranches offered a compelling yield pickup in the low double digits, above historical equity returns. This created an attractive risk-reward opportunity for portfolios that could take a tactical position in this area and in the right structure.

Despite exposure to similar underlying assets, mezzanine CLO debt was more attractive than direct lending, high yield, and bank/leveraged loans. Leveraged loans and direct lending strategies had higher historic default rates and, in our opinion, had more embedded risk.

Active Management and Risk: A Track Record of Resilience

Most CLOs are actively managed by professional portfolio managers. During the reinvestment period (typically 3-5 years), managers trade loans to maintain credit quality and diversify the portfolio. This active management allows for the adjustment of the loan portfolio in response to changing market conditions, contributing to the historically strong performance of CLOs. Managers can sell riskier loans and reinvest in more stable ones, ensuring the CLO maintains its credit quality.

Even during financial crises, CLO debt tranches performed better than many fixed-income investments. For instance, during the 2008-09 financial crisis and the 2020 COVID-related market shock, CLO debt tranches showed resilience with low default rates. It is important to note that CLOs are not the same as mortgage collateralized debt obligations (CDOs), which contributed to the 2008-09 financial crisis.

In brief, CLOs provide unique advantages for high-net-worth portfolios (if appropriate) but are just one aspect of a well-balanced portfolio—one that may not be permanently attractive. As a unique and nuanced asset class, CLOs require thorough understanding and professional guidance to maximize benefits and mitigate associated risks.

CM Wealth Advisors LLC is an SEC-registered investment advisor under the Advisors Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. Form ADV Part 2A can be obtained by visiting https://adviserinfo.sec.gov and searching for our firm name. ADV Form 2B is available upon request.

This has been provided for informational purposes only and is not intended as legal, tax, or investment advice, or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of publication and are subject to change without notice. Past performance is not indicative of future results.

All investments involve risk, including loss of principal, and there is no guarantee that investment objectives will be met. It is important to review your investment objectives, risk tolerance, and liquidity needs before choosing an investment style or manager. Investments are subject generally to market, market sector, market liquidity, issuer, and investment style risks, among other factors, to varying degrees.

Investors in CLOs generally receive payments that are part interest and part return of principal. These payments may vary based on the rate at which loans are repaid. Some CLOs may have structures that make their reaction to interest rates and other factors difficult to predict, make their prices volatile, and subject them to liquidity and valuation risk. Investments in bonds and other fixed-income instruments are subject to the possibility that interest rates could rise, causing their value to decline. Investors in asset-backed securities, including mortgage-backed securities, collateralized loan obligations (CLOs), and other structured finance investments, generally receive payments that are part interest and part return of principal. These payments may vary based on the rate at which the underlying borrowers pay off their loans. Some asset-backed securities, including mortgage-backed securities, may have structures that make their reaction to interest rates and other factors difficult to predict, causing their prices to be volatile. These instruments are particularly subject to interest rate, credit and liquidity and valuation risks. High yield bonds may present additional risks because these securities may be less liquid, and therefore more difficult to value accurately and sell at an advantageous price or time, and present more credit risk than investment-grade bonds. The price of high yield securities tends to be subject to greater volatility due to issuer-specific operating results and outlook and to real or perceived adverse economic and competitive industry conditions. Bank loans, including loan syndicates and other direct lending opportunities, involve special types of risks, including credit risk, interest rate risk, counterparty risk, and prepayment risk. Loans may offer a fixed or floating interest rate. Loans are often generally below investment grade, may be unrated, and can be difficult to value accurately and may be more susceptible to liquidity risk than fixed-income instruments of similar credit quality and/or maturity.